The report titled “India EV Charging Equipment Market Outlook to FY’2026 – Driven by Increasing Adoption of Electric Vehicles along with Implementation of FAME II Policy by Government” provides a comprehensive analysis of the potential of Electric Vehicle Charging Equipment industry in India. The report covers various aspects including the current EV Scenario and charging infrastructure status in India, revenue generated from EV Charging equipment, its segmentations viz Type of Charger – Fast (DC) vs. Slow (AC), Type of Charging Stations, Application (4W vs. 3W vs. 2W), Geographic Distribution, Distribution Channel and By Organized and Unorganized Sector, major trends and development, issues and challenges, government regulations and product analysis. The report concludes with market projections for future of the industry including forecasted industry size by revenue along with analyst recommendations and key market opportunities.

India Electric Vehicle Charging Equipment Market

India Electric Vehicle Charging Equipment Market

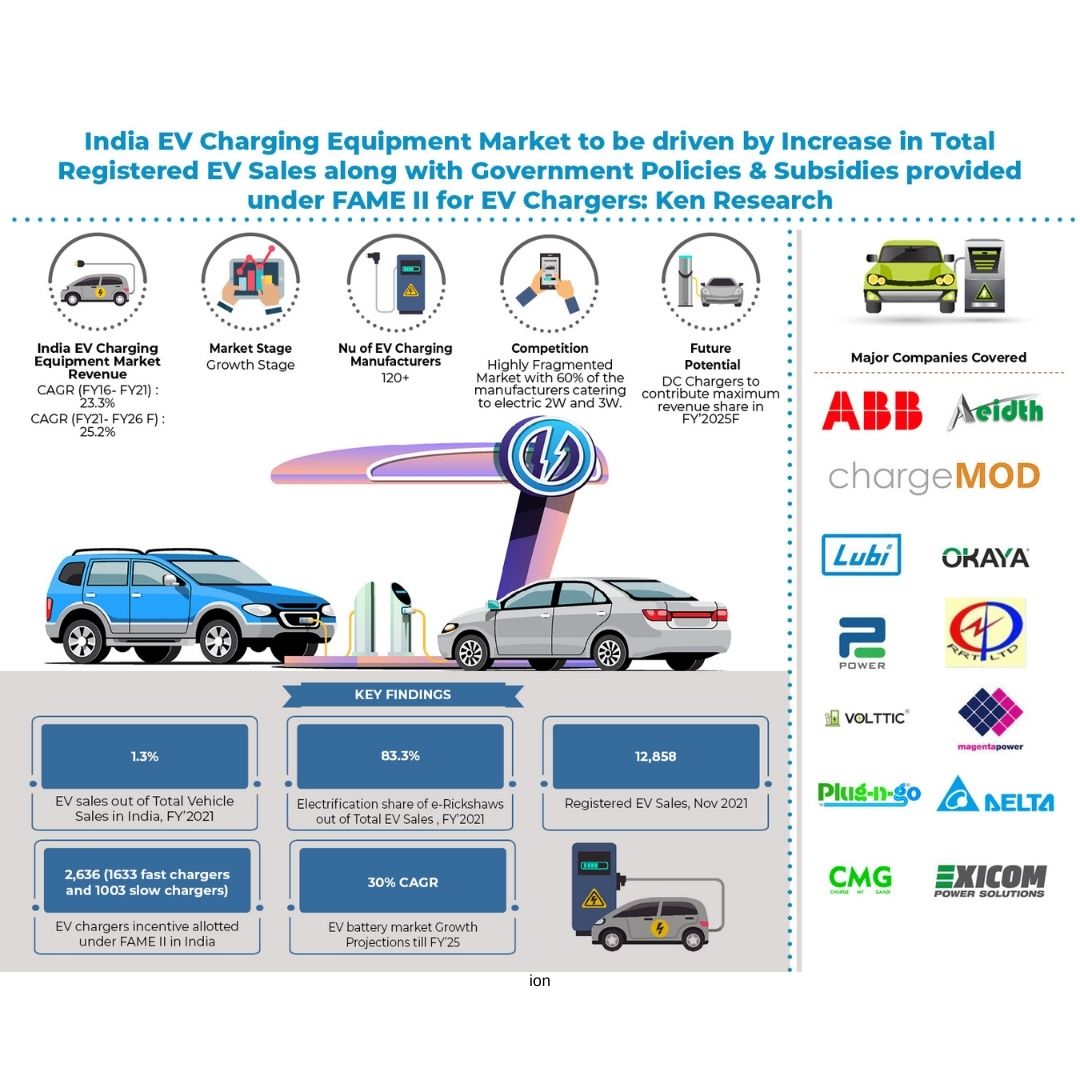

India, the world’s 6th largest economy by nominal GDP and the 3rd largest by PPP, is characterized as a middle-income developing market economy. 2- and 3- Wheelers that account for close to 50% share dominate the Indian urban mobility modal share. EVs are slowly gaining traction with less than 2% of vehicles deployed as EVs in India. The charging infrastructure in India is currently quite under-developed with as many as 26 EVs percharger available in the country, compared to only 8 in China and 17 in the US. There are ~300 community charging stations in India, of which 22 were fast-charging points in 202. However, India EV Charging Equipment Market gained significant momentum after the implementation of FAME India scheme. The Department of Heavy Industry (DHI) also planned to incentivize 1,000+ charging stations with 6,000+ chargers, which is the major growth driver for the market. Lack of Space, Infrastructure and Manpower for Setting-Up along with High Initial Cost of Charging Equipment and Installation are the major challenges in India EV Charging Equipment Market.

India Electric Vehicle Charging Equipment Market Segmentation

By Type of Charger – Fast (DC) vs. Slow (AC): Majority of the revenue from the EV Chargers in India in FY’21 are generated from DC Chargers offering advantages in situations where quick battery replenishment is either required or preferred. AC Chargers are ideal for charging at home or work because it needs more time to load whereas DC fast chargers may be found on highways or other locations where an EV might require a quick charge-up in minutes.

By Type of Charging Stations: Portable Chargers contributed the highest revenue share of FY’21 followed by Public and Private Charging Stations. There are no fixed categories and some charging facilities may demonstrate hybrid characteristics. For instance, charging infrastructure owned by EV fleet owners/operators for captive use is considered private, but it can be opened to the public as a paid charging service when fleets are in circulation.

By Application (4W vs. 3W vs. 2W): 2W have relatively small batteries (2–3 kWh) which often are removable to enable home and office charging from a standard wall socket. 3W slightly larger batteries (8–12 kWh) and come in variations with fixed and removable batteries. 4Ws come with various sizes of batteries and utilize different charging standards as determined by the OEM.

By Geographic Distribution: Southern India leads the EV Charging market currently, followed by North and West. Eastern India continues to be an unexploited potential area for EV Charging due to terrain constraints.

By Distribution Channel: Market is dominated by the unorganized players capturing majority of the overall market share in terms of revenue with the direct sales process.

India Electric Vehicle Charging Equipment Market Competition

The market is highly fragmented with presence of major private and public entities setting up charging infrastructure in various potential locations across India. Different types of EV Chargers are available in the Indian Market comprising of Type 1, Type 2, AC and DC, unidirectional and bidirectional charging catering to e4W, e3W as well as e2W. While EESL stands out in the race, owing to its bagging of all the major contracts under FAME I scheme and being a public entity, other companies such as ABB, Fortum, Aeidth, EESL, Ather Energy, Volttic, Charge+Zone are also the key players in the market. To be price competitive and reduce the risk that comes from the mere sale of energy, CPOs may need to explore partnerships and adjacent offerings.

India Electric Vehicle Charging Equipment Market Future Outlook and Projections

India EV Charging Equipment Market is expected to generate substantial revenues owing to increase in market penetration of EVs and surge in government initiatives for development of EV charging infrastructure. With the right government policies, a local supply chain, lower battery prices and widespread charging infrastructure, the EV market could contribute $6.4 Bn in next 5 years. eRickshaws, eAutos, and e2Ws are the most promising segments for electrification in India and are expected to account for more than 4 million units by 2025. Further, limited number of EV charging stations, lack of standardization of EV charging, rise in demand for luxury and feature enabled vehicles, and wireless charging for EVs to have strong impact on the market.